Given the banking, currency, and debt crises in #Lebanon, below is a thread about various options for depositors in Lebanese banks. This is by no means personal advice or recommendations – just a basic analysis of the different options.

The basic problem is that majority of deposits are denominated in USD. Banking system is out of USD. Local currency, LBP, pegged to the USD for past 25 years at 1500, is now around 4000. Essentially, all current deposits are defacto in LBP & being converted at “official” rates

Official USD rates that banks convert your cash withdrawals at are much lower than market rates. They are also arbitrary and subject to change and are limited by amount in local currency.

To summarize the problem: depositors have life savings in a quickly depreciating currency held at insolvent banks that they can only cash out in limited amounts and convert at a disadvantageous rate.

The goal is to transfer deposits into assets that will appreciate – or more realistically – depreciate less than the LBP given that Lebanon will be in a deep recession for an uncertain time; ** with the least impact on your lifestyle & consumption preferences**

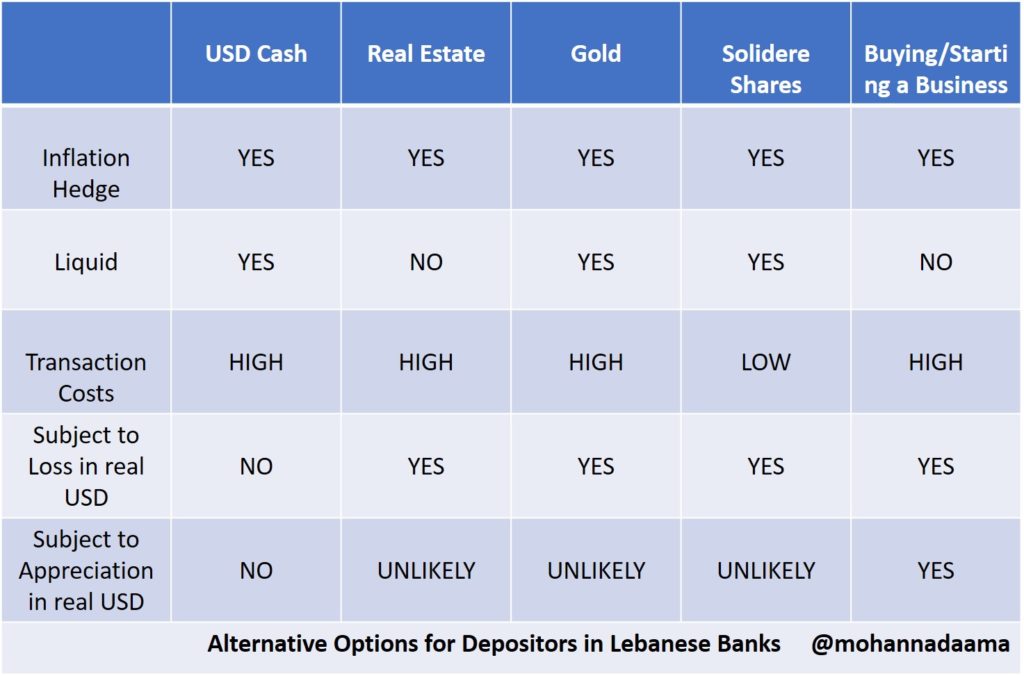

I will limit the options to 5 broad categories that are relatively widely available in Lebanon. USD bank notes, Real Estate, Gold, Equity shares in the local stock market, let’s say Solidere, and buying or starting a business.

To best evaluate these options, we have to look at 3 primary characteristics: Is it a hedge against inflation and a devaluing LBP? Is it liquid? and are transaction costs low or high?

Before I analyze each, it is important to note that the set of options should not be the same for all depositors. Small depositors are probably best off with converting to USD bank notes but that is not practical for large depositors – certainly not for all their deposits.

USD Bank notes are a great inflation hedge; very liquid & will not go down in value in real USD terms. Downside is the high transaction costs involved. Withdrawing LBP at a disadvantageous rate, then converting to USD at exchange houses at market rate will involve a haircut.

Real Estate is a good inflation hedge but is not liquid and involves high transaction costs to buy and to sell. It is also subject to a decrease in value in real USD terms given the local economy. Least impacted real estate is class A properties in super prime locations.

The equation with real estate is that we know it is overvalued today but will it go down in value more than the depreciation in Lira – particularly if you are able to use your current deposit via a banker’s check? I can see scenarios where Lira can go down 10x in value but not certain properties. So, some particular type of real estate may be a good idea.

Gold is certainly an inflation hedge, especially in LBP. However, buying it involves two high hurdles: transferring your deposit to real dollars & then buying gold at a premium to its spot price. You are already 2 steps behind; & later you sell it at a discount to spot price

Equities are generally a good hedge against inflation but majority of listed shares on the Beirut stock exchange are those of the troubled banks. Solidere is biggest listed company and holds prime real estate. Started the year at $7, now near $11

Solidere shares are relatively liquid, trade in USD, can be bought easily with low transaction costs and its real estate holdings are, in theory, an inflation hedge. However, land prices and rents are expected to plummet along with the economy.

The best thing going for Solidere shares is that they are easy to buy and sell. Many will use it as an alternative bank account and sell shares as needed. Regardless of the company’s fundamentals, this will make its shares in MUCH greater demand than otherwise.

The biggest opportunity for captive deposits is starting a new business. Export-replacement and export-focused businesses should thrive during the next period. There will be existing businesses that will be, sadly, sold by those fed up and bent on emigrating

There will also be many new business opportunities in export-replacement/focused businesses. Lebanon’s economy will change and those who step in front of new opportunities will gain the most. Won’t be risk-free but will have the most upside potential!

Making money the easy way via your bank account is gone forever. Taking measured risks and seizing new opportunities will be the way to make excess returns in the future. Large depositors will likely diversify among those 5 options I listed.

None of these options offers guaranteed returns. Depositors will likely lose some of their principal on all of these options. Starting a business is the only option that gives meaningful potential appreciation. /end